The largest IPO in history will thrill the markets, but behind SpaceX lies a vast wager on America’s entire strategic future.

Not to sound blasphemous, but in the world of capitalist economics, where the market is sometimes treated almost like a religion, a grand IPO (initial public offering) tends to be received as both prophecy and confirmation of faith. It is a "happy moment," euphoric by design: a vast company whose very existence is supposed to prove the efficiency of modern private enterprise — in this case, a claim questionable in every respect — finally goes public, and everyone is invited to take part, share in the joy, and buy into the success. That is the convenient story offered to the public. Behind it, however, a very different reality is taking shape.

Something very much like that spectacle awaits us in a few days — on June 12, to be precise. We are, of course, talking about Elon Musk’s SpaceX. This public listing offers rockets, satellites, artificial intelligence, and American geopolitical hope in a single package. But behind the largest IPO in history lies a question that goes beyond both Musk and Wall Street: who will pay the price if the new space euphoria turns into a bubble?

The Largest IPO in History and the Price of the Future

What is usually sold on the stock market is a share. Sometimes, however, something much larger is being sold: the feeling that you are entering history before everyone else. That is the dream behind every IPO campaign, and such campaigns are prepared years in advance.

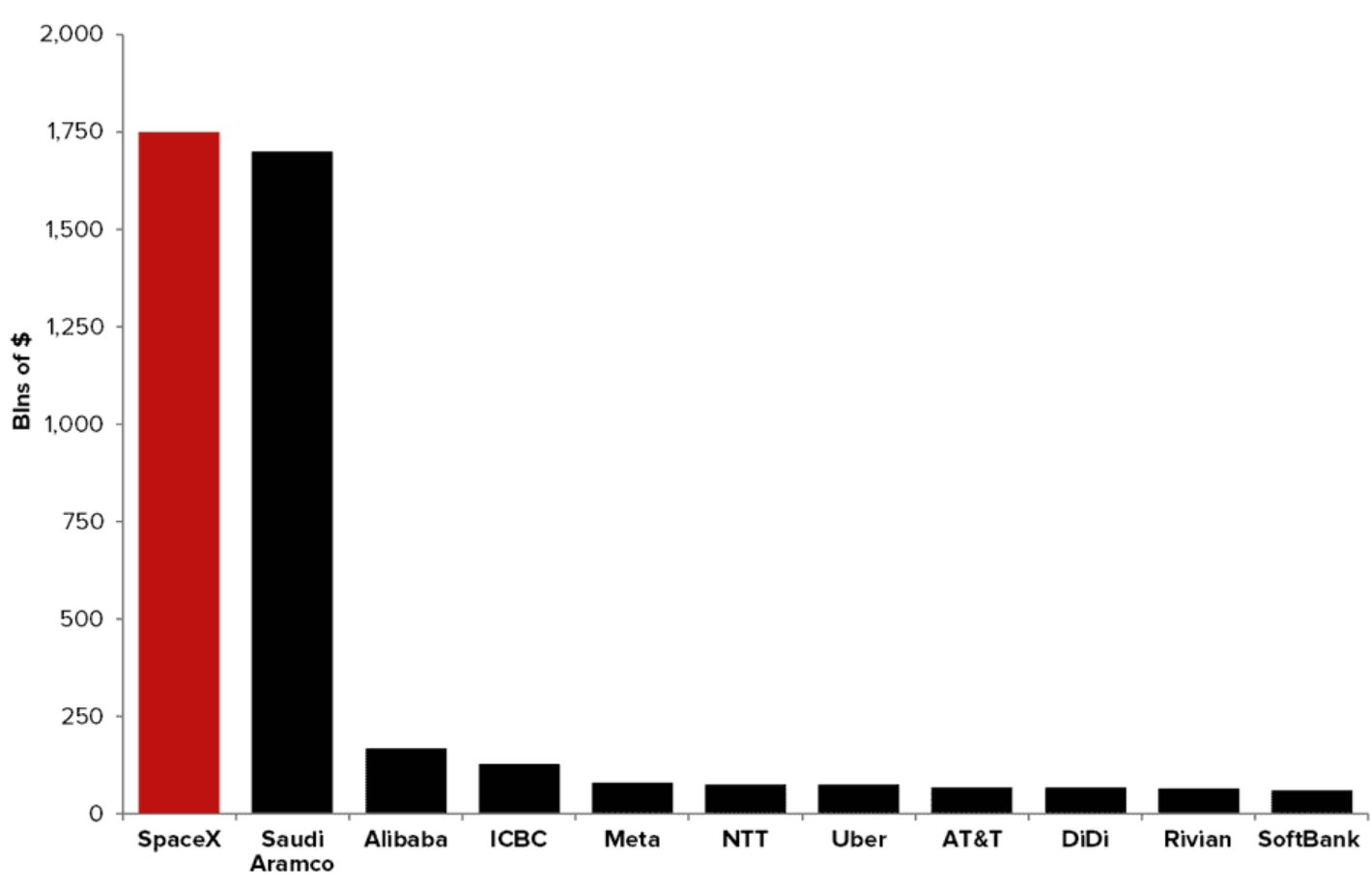

Elon Musk’s company is trying to raise around $75 billion through its initial public offering. At first glance, that figure sounds enormous, but by itself it does not tell us how the market is actually valuing SpaceX. The key number is the other one: roughly $1.75 trillion. That is the implied value of the entire company if the shares are sold at the planned price. In other words, SpaceX is not selling its whole empire. It is selling only a small piece of it, while using that sale to assign a public market price to the empire as a whole.

Let us spell this out.

If $75 billion is measured against a valuation of $1.75 trillion, the IPO represents roughly 4 to 5 percent of the company’s total value. That is a small stake, but large enough to create an enormous market effect. By selling a relatively narrow block of shares, SpaceX can raise more capital than many states could raise through serious budget reforms, while existing owners and Musk’s management structure retain almost complete control of the company.

This is a crucial part of the story and deserves emphasis: an IPO is not merely a way for a company to raise money. It is also a public ritual of valuation. If investors accept a price that values SpaceX at $1.75 trillion, that valuation becomes a reference point for every future discussion of the company: employee shares, existing investors, future sales, borrowing, and also SpaceX’s political weight and its place in the American strategic narrative, especially now that big space business and America’s survival are entering into symbiosis.

If someone sells 4 percent of a house for $75 billion, the market is accepting the claim that the entire house is worth around $1.75 trillion.In that sense, the IPO could be described as a "test of an assumption." A small portion of the company is offered to the market. If investors embrace it enthusiastically, the company gains an argument that its valuation is not merely the presentational ambition of investment banks, but a market-confirmed price. If demand greatly exceeds supply — and it will — an even more favorable message emerges for SpaceX: perhaps even $1.75 trillion is too low for what investors believe they are buying.

According to available reports, investor demand has already reached around $150 billion. That means investors are currently showing interest in roughly twice as many shares as are being offered. In smaller "hot IPOs," such a ratio might not sound spectacular. But for an offering of this size, demand at twice the available supply means something else. The market is not merely expressing interest in a stock; it is showing a willingness to participate in the "creation of the price" for one of the key companies of America’s future. The real price? That remains to be seen.

Put even more simply: if someone sells 4 percent of a house for $75 billion, the market is accepting the claim that the entire house is worth around $1.75 trillion. SpaceX’s IPO does exactly that. It is not selling the whole house. It is selling a small window through which a price is assigned to the entire structure. That is precisely why this offering has such power. A small stake can become the mechanism for a colossal public valuation, while real control remains in the hands of the founder and existing owners.

And yes, it is striking that even such a small portion of the company — around 4 percent — would itself constitute the largest IPO in history. The previous record belonged to the Saudi state oil giant Saudi Aramco, which in 2019 initially raised $25.6 billion by selling 1.5 percent of the company at a valuation of around $1.7 trillion. Later, after an additional share-sale option was exercised, the total value of Aramco’s IPO rose to around $29.4 billion. SpaceX is now trying to raise around $75 billion, more than twice Aramco’s expanded record. The difference is as politically interesting as it is financially immense. Aramco brought a small piece of the Saudi oil empire to market, a symbol of old energy power. SpaceX is bringing a small piece of the American orbital empire to market, a symbol of new strategic infrastructure. One record belonged to oil. The other belongs to space. America is excited, seeing in this a continuation of its global — indeed, beyond-global — dominance.

SpaceX is not a "pump and dump" scheme, not a scam designed for quick profit. The company is bringing real rockets, real satellites, and real contracts to the market. But it is also bringing something even more attractive to investors than current earnings: the promise that it will control the infrastructure of the future — launches, satellite internet, military communications, data, artificial intelligence, and perhaps even part of the computing infrastructure above the Earth.

That is why SpaceX’s IPO cannot be reduced to ordinary market euphoria. It is the financial packaging of the future. The market is not merely buying a company here; it is buying the right to participate in the privatization of a new layer of what is being presented as civilizational infrastructure.

A Real Rocket and a Financial Fantasy Can Fly Together

The obvious must be acknowledged. The company has accomplished what traditional state programs and old military-industrial contractors often did more slowly, more expensively, and more sluggishly. SpaceX has dramatically changed the economics of launches, developed reusable rockets, and created Starlink, a satellite internet network that already has global strategic importance — often as part of American hegemony as well (inticing protests in several countries).

SpaceX is certainly not a "pump and dump," nor is it a paper company without products. Its presence in orbit is visible to the naked eye in the night sky. Moreover, its importance — or its danger, depending on one’s perspective — in communication networks is visible in wars, crises, and remote areas where conventional infrastructure either does not exist or no longer functions. At the same time, it should be remembered that SpaceX was built not only by Musk but also by enormous American state subsidies, which shows that this is not exactly a "pure capitalist fairy tale." Such stories rarely are. A great deal of the "socialist model" is built into SpaceX as well — in the economic sense, of course. Built into the state side of the project is the idea of America’s military and technological survival; not only survival, but the continuation of dominance. SpaceX was tied to that from the beginning. Musk knows it too, although he will wisely remain silent about certain details, or emphasize them when useful — for instance when speaking of SpaceX’s influence on the Gulf or Ukrainian fronts: from drone navigation to AI, satellite intelligence, and so on.

SpaceX is real, enormous, and aimed at the future. Yet that is exactly why a potential "bubble" becomes more dangerous. The largest financial bubbles do not form around empty inventions. They form around real technological breakthroughs to which the market then assigns a euphoric, almost infinite future.

The dot-com era was one such example. The internet, obviously, really did change the world. Yet many internet stocks still destroyed capital and burned through investors’ money. Railways in the 19th century also transformed the economy and industry. But speculative waves, bankruptcies, and crashes formed around them too. The lesson keeps repeating itself: the reality of a technology, even one that will define the future, does not protect investors from the madness of price.

The emergence of artificial intelligence will without question define humanity’s future; that scenario is already locked in. But that does not mean that all the major companies now bringing it to market will not perhaps collapse under the weight of expectations.

SpaceX is an ideal object of financial mythology. It is real enough that critics can be accused of "not understanding the future." It is futuristic enough that almost any valuation can be made to sound insufficiently ambitious — and this IPO will demonstrate precisely that. All of this makes it an ideal vehicle for the creation of a vast modern technology bubble.

Because a valuation of roughly $1.75 trillion means the market is already pricing in a whole series of future "victories." It is a price that assumes SpaceX will maintain its dominant position in launches, expand Starlink, open new markets, withstand regulatory pressures, control capital costs, and turn the vision of space-based artificial intelligence into a real business model. And the competition? And China? China is not even mentioned, lest it spoil the IPO celebration. We will return to that shortly.

Each of those assumptions may make sense on its own. Taken together, however, they raise the question financial euphoria prefers to avoid: how much "future" can be built into today’s price before investment becomes faith?

AI in Orbit and the New Religion of Valuation

The most interesting part of the SpaceX story is not merely the rockets. Rockets have become the ticket into a much larger narrative. The company is selling investors an image of a market in which space becomes a platform for artificial intelligence, data centers, and computing capacity above the Earth.

Capital imagines orbit as a space without politics, without unions, environmental permits, or local resistance.The story sounds almost perfectly suited to our time. Artificial intelligence requires enormous amounts of electricity, chips, cooling, and space. American infrastructure is struggling to keep pace with the hunger of data centers — while also, among other things, trying to dump them on others; see: The Cloud Has Fallen to Earth and Is Swallowing Everything in Its Path:

On Data Centers and the Degradation of Societies Left in the Dark. Doing business on "Earth" is becoming complicated. Permits take time. Energy grids are buckling under pressure. Local communities are increasingly asking questions about water, electricity, and ecology.

In this story, space appears as an elegant, graceful escape from terrestrial constraints.

Solar power without night. Orbital infrastructure without local laws or regulations. Data centers without neighbors protesting over water and electricity consumption. Capital imagines orbit as a space without politics, without unions, environmental permits, or local resistance.

This is what financial religion looks like. Every real technical problem becomes a potential market: find a problem, find a solution, get rich. Then every potential market becomes a presentation, and every presentation becomes a valuation. The investor is then offered the chance to pay today’s price for a future that does not yet have any stable form.

Space-based data centers may be a serious technological subject, and their importance should not be dismissed. Data processing in orbit already makes sense in satellite systems, Earth observation, and military applications. But enormous orbital computing capacity for artificial intelligence brings with it a very different set of problems. Launching equipment, maintenance, replacing components, communication delays, security, failures, and the cost of capital are not details. They are the modern gears without which the machine does not run.

The market, however, often behaves as if the gears can come later. The narrative always comes first.

Capitalism has literally subordinated everything to its own purpose: everything around us, from housing and attention to parenthood, religion, life, and death — everything. Now it is treating orbit as the next layer of accumulation.

China Builds Factories, America Sells Orbit

The geopolitical background gives the whole story even greater weight. For decades, the United States relocated much of its material production beyond its own borders. What it retained was the dollar, Wall Street, software, the largest technology companies, and military supremacy. China, during the same period, built manufacturing depth, industrial chains, ports, batteries, solar panels, shipbuilding, and an increasingly ambitious space program.

That division defines our era. China has factories. America has financial markets, the military-technological complex, and companies that promise control over the highest layers of infrastructure. SpaceX fits perfectly into this model. It is a private company that grows on state contracts, military relevance, technological dominance, and the market myth surrounding its founder.

SpaceX’s Chinese Rivals

China does not have a single "SpaceX of its own," but it does have an entire space ecosystem in which state companies, locally supported technology projects, and a new generation of private launch firms overlap. This is an important difference between the American and Chinese models. In the United States, enormous symbolic and market weight is concentrated around one private company and one founder. China is building multiple parallel capacities that, taken together, are intended to produce a similar strategic effect.The most visible Chinese answer to Starlink is Qianfan, also known as Thousand Sails or the Spacesail Constellation. Behind the project stands the Shanghai-based SpaceSail structure. It is a megaconstellation of low-Earth-orbit satellites intended to provide satellite internet and create a Chinese alternative to Starlink. According to available plans, Qianfan should eventually contain more than 15,000 satellites, while the number already launched is rising rapidly month by month.

Alongside Qianfan, there is also Guowang, or SatNet, a state-directed project for a national satellite internet network. If Qianfan is the most visible Chinese answer to Starlink in a commercial sense, Guowang is its strategic state shadow. It is planned as a vast network of several thousand satellites that would give China its own global communications layer in low orbit. In a world where satellite internet increasingly also means military resilience, control of data, and communications autonomy, such networks are not merely technological projects. They are infrastructures of sovereignty.

In rockets and launch systems, the Chinese company closest to being a SpaceX rival is LandSpace. This private company is developing Zhuque-3, a reusable rocket often compared with Falcon 9. LandSpace has not yet reached the level of reliability and launch frequency that SpaceX has built over years of experience, but it shows the direction of Chinese ambition. China knows that megaconstellations such as Qianfan and Guowang require cheap, frequent, and reliable access to orbit. Without reusable rockets, mass satellite internet cannot be delivered at a price capable of competing with Starlink.

Through SpaceX, the United States is trying to show that it can still produce something complex and strategically irreplaceable.

The American answer to the Chinese industrial state takes a very specific form here. The state — in this case, the American state — provides contracts, accelerates permits, and defines space as a realm of national security. The private company develops the technology and keeps the ownership. Wall Street converts a future monopoly into today’s price. This is the political economy of the American model in its purest form.

The Skeptics Come from the Very Heart of the System

Skepticism toward SpaceX’s IPO does not come only from circles that criticize Musk. In fact, those whose entire argument amounts to "I don’t like Musk" often have little of substance to offer. But substantive arguments do exist.

Denmark’s AkademikerPension, an academic pension fund, has already placed SpaceX on its exclusion list. That is an important signal because a pension fund has a different task from a hedge fund. A hedge fund can seek a short-term jump in price. A pension fund manages people’s deferred wages* — people who expect security in old age. When such an institution warns about valuation and corporate governance, that is not simply "resistance to Musk"; it is a warning about the relationship between risk and price.

Clearly, the concentration of power around Elon Musk cannot be ignored. If one man retains dominant voting rights while also holding key managerial functions, public investors are buying only a minority stake in a structure in which their ability to exercise oversight is very limited. The stock market is then presented as a democratization of ownership, while real control remains closed.

Aswath Damodaran, a professor of finance at NYU Stern and one of the world’s best-known valuation experts, is also an important part of this story. His estimate of SpaceX’s value is lower than the targeted IPO valuation, particularly because he is cautious about the enormous market assumptions tied to artificial intelligence.

Morningstar, an independent investment research firm, has gone even further and estimated SpaceX’s value at around "only" $780 billion, less than half the targeted IPO valuation.

The problem arises when a very expensive and highly euphoric company enters a major index. At that point, it is no longer bought only by investors who have voluntarily concluded that the price is reasonable. It is also bought by funds that must follow the rules.The warning related to index funds is especially interesting, because here the story leaves the world of professional investors and enters, among other things, the pensions of ordinary people.

An index, in the simplest terms, is a list of stocks that together represent a particular part of the market. The best-known American example is the S&P 500, an index that tracks 500 large American companies. When people say "the market went up," they often really mean that one of these indices went up.

An index fund is a fund that does not try to cleverly pick individual stocks — this bears repeating, and emphasizing again. It simply tracks an index. So if Apple is part of the index, the fund buys Apple. If Microsoft is part of the index, the fund buys Microsoft. If a new company enters the index, the fund literally has to buy it in order to keep faithfully tracking that index. Put simply: if someone "gets into the 500," they get bought. This is so-called passive investing. It is popular because it is cheap, simple, and often more successful over the long term than expensive fund managers trying to beat the market.

The problem arises when a very expensive — and very euphoric — company enters a major index. At that point, it is no longer bought only by investors who have voluntarily concluded that the price is reasonable. It is also bought by funds that must follow the rules. In other words, they cannot suddenly invent some kind of S&P 499 because they fear SpaceX is a bubble.

Their decision, then, does not arise from an assessment that the stock is cheap, safe, or a wise purchase. It follows simply from the index methodology itself. The stock becomes a mandatory item in the portfolio.

For the ordinary saver, this means something very concrete. A person may have retirement savings, an investment fund, or an account that automatically invests in a broad American index. They may never have decided to buy SpaceX. They may never have read the IPO prospectus. They may not care at all about Musk, space, or Starlink. But if SpaceX enters a major index, part of their savings can easily end up in that stock because the fund follows the rules of the index.

This raises a question far broader than SpaceX. Who writes the rules of the index? Who decides when a new megacompany becomes important enough to enter the portfolios of millions of people? Who bears the risk if the price proves inflated? Financial markets like to speak of free choice, but passive investing often turns choice into an automatic mechanism.

Here lies the hidden political economy of index funds. On the surface, they appear neutral and technical: buy the whole market, do not try to be smarter than everyone else, let time work for you. In practice, someone still decides what "the market" is. Someone sets the rules for entering and leaving the index. Someone decides whether a new technology star will become a compulsory component of retirement savings.

If SpaceX enters such a mechanism at an extremely high price, the risk spreads far beyond the circle of people who consciously wanted to participate in the space wager. The stock is then no longer merely an object of enthusiasm, greed, or geopolitical optimism. It becomes part of the financial infrastructure of everyday life. That is the moment when stock-market euphoria turns into a broader social risk.

Pension Money as Fuel for the Space Bet

The deepest risk of SpaceX’s IPO is not found only in the share price. It lies in the question of whose money is being used to sustain that price.

If SpaceX succeeds, big capital, early investors, and the founding power structure will reap extraordinary gains. If the price collapses, the loss may spill through funds, indices, and the savings accounts of ordinary people.Let us briefly explain pension funds. Pension funds do not manage abstract capital. They manage "deferred wages." Part of today’s labor is converted into financial assets with the promise that tomorrow they will pay for rent, medicine, food, and a dignified old age. When that money is poured into megadeals filled with euphoria, risk is shifted from professional speculators to people who often have no idea what is in their portfolios.

This is also the class dimension of the story. If SpaceX succeeds, big capital, early investors, and the founding power structure will reap extraordinary gains. If the price collapses, the loss may spill through funds, indices, and the savings accounts of ordinary people. In other words: gains are concentrated, risks are dispersed. Or, more simply still: if the thing succeeds, the rich become much richer; if it fails, the poor carry the burden.

Scandalous? But that is how it is. That is how mature financialization works. First, the future is turned into a story. Then the story is turned into a valuation. The valuation enters an index. And in the end, the worker discovers that their pension money had already been taking part in the risk.

The American Pension Tied to the Stock Market

In America, the pension system is deeply tied to the S&P 500, most often indirectly through 401(k) plans — the name comes from Section 401(k) of the U.S. tax code — IRA accounts, index funds, and target-date funds, meaning retirement funds calibrated to the expected year of retirement. Not every American pension is automatically invested in the S&P 500, but that index is one of the main gravitational centers of American retirement savings.The most important channel, which you have surely heard of, is the 401(k): a private retirement account that many workers hold through their employer. The worker sets aside part of their wages, the employer often adds a contribution, and the money is invested in funds offered within the plan. Those funds very often include U.S. equity funds, S&P 500 index funds, broader total-market funds, or target-date funds that themselves have heavy exposure to U.S. equities.

According to the Investment Company Institute, at the end of 2025, 401(k) plans held around $10.2 trillion in assets, while mutual funds managed around $5.8 trillion, or 57 percent of the assets in 401(k) plans. Of that, equity funds held around $3.4 trillion, showing how deeply American retirement savings are tied to the stock market.

SpaceX thus becomes a symbol of a wider order. Capitalism is no longer seeking only new markets on Earth. Housing has been financialized. Health care is a market. Education is debt. Attention is a commodity. Data is raw material. The next frontier lies above the atmosphere.

SpaceX may indeed be opening a new era of access to space. Through SpaceX, the American state may gain a strategic advantage in its rivalry with China. All of those claims can stand at the same time as another one: the price may be too high.

The stock market loves moments in which the future appears inevitable. Such moments create the greatest narratives and the most expensive mistakes. SpaceX’s IPO should therefore be seen as a technological event, a geopolitical bet, and a test of the social distribution of risk.

The rockets are heading for orbit, but the balance sheet remains on Earth. And the bill, as so many times before, may end up with those who were never even invited to the launch.

Sources

- Aol.com The SpaceX IPO Is Just Days Away. History Says the Stock Will Do This When It Starts Trading. https://www.aol.com/articles/spacex-ipo-just-days-away-090800373.html

- Finimize.com SpaceX’s IPO Is Testing Wall Street’s Playbook https://finimize.com/content/spacexs-ipo-is-testing-wall-streets-playbook

- Fortune.com Top analyst has harsh words for SpaceX debut: ‘We recommend that investors avoid this IPO’ https://fortune.com/2026/05/29/spacex-ipo-should-i-buy-bear-case-david-trainer/

- Pionline.com Pension funds call SpaceX governance ‘reckless’ as forced buying looms ahead of IPO https://www.pionline.com/institutional-investors/pension-funds/pi-elon-musk-spacex-ipo-index-pension-funds/

- Responsible-investor.com To be able to copy & paste content to share with others please contact us at [email protected] to upgrade your subscription to the appropriate licence https://www.responsible-investor.com/spacex-ipo-plans-trigger-pension-fund-governance-concerns/

Comments