In the months ahead, one number is worth watching: it tells us not just where markets are going, but how long America can afford to sustain its power.

United States Treasuries may be the most boring financial instruments in the world. That is exactly why we should pay attention when they become interesting. They do not carry the drama of tech giants’ shares, they do not promise overnight riches, and they do not produce the euphoria of the crypto market. Their function is almost the opposite: to serve as the quiet background of the system, the foundation on which everything else is built. But when that foundation starts to tremble, it is a sign that the price of the American order itself is changing.

That is why, in recent months, we have increasingly heard the warning that one should watch the American "10-year", meaning the yield on the 10-year U.S. government bond, and that if it crosses 5%, a serious problem begins. But why is that so? What does this number actually reveal, and is it really powerful enough to say that, "at 5%", Trump’s armada in and around the Persian Gulf would have to start sailing back home? Today we will look at that in detail.

The theory is not wrong, but it is somewhat simplified. 5% is not a magic number after which the system automatically breaks. But it is a major psychological threshold. It is the moment when the market begins asking, more loudly, the question that has been suppressed for years: how much does it actually cost to maintain the American state, American debt, and therefore American global dominance?

When people say "10-year bond" in everyday language, they usually mean the 10-year U.S. Treasury note, a government debt security with a maturity of 10 years. Technically, just to mention it because the terminology can be confusing, the U.S. Treasury calls securities with maturities of 20 or 30 years "bonds", while those with maturities of 2, 3, 5, 7 and 10 years are "notes", although in public language that distinction is often erased.

How does all of this work? Without going too deeply into the mechanics again, the essence is simple: an investor lends money to the U.S. government, the government pays interest every six months, and at maturity repays the principal. These 10-year notes are officially issued with a fixed interest rate and can be held until maturity or sold earlier on the market.

If the U.S. Treasury is the "safest asset in the world", then everything else has to offer a higher yield because it carries more risk.But what the market watches every day is not only that initial interest rate. It watches the yield. The yield is the effective return an investor receives by buying the bond at its market price. Here, a rule applies that sounds paradoxical but is crucial: when the price of a bond falls, its yield rises. This is extremely important to understand. If investors sell U.S. bonds en masse, their price falls, and when the government issues new debt, it has to offer a higher return, a bigger "bonus", to attract buyers. In other words, rising yields mean that money is becoming more expensive - not only for Washington, but for the entire economy built around the American financial system and the dollar.

That is why the 10-year yield is so important. It is the benchmark price of long-term money. Mortgages, corporate loans, stock valuations, pension funds, and even financial conditions in countries far from the United States are indirectly tied to it. Put it this way: if the U.S. Treasury is the "safest asset in the world", then everything else has to offer a higher yield because it carries more risk. Because when that "safe" asset itself starts offering around 5%, the investor logically asks: why would I enter overpriced stocks, risky corporate bonds, or the debt of weaker states if Washington is already paying me that much? For an investor, especially one who is not chasing huge returns but merely wants, say, protection from inflation, 5% sounds very good.

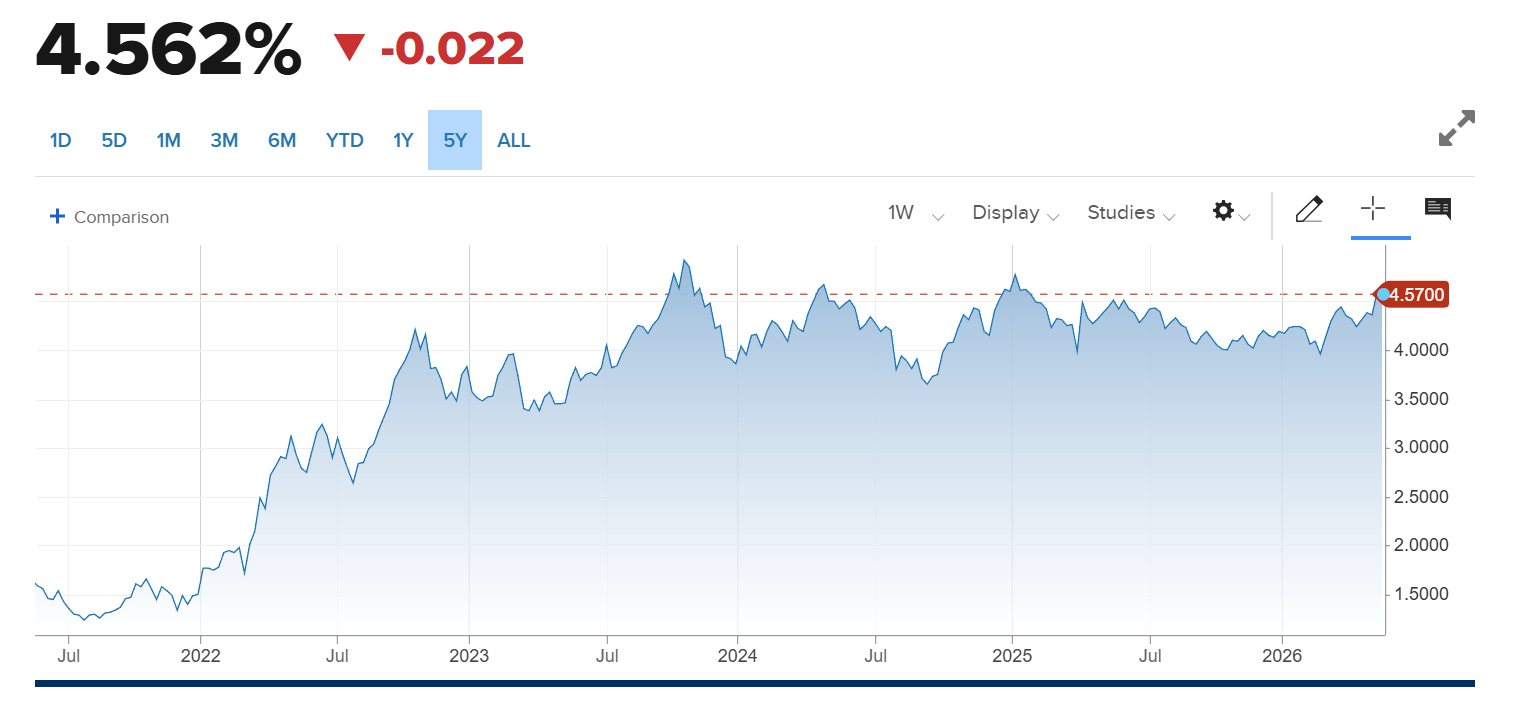

According to data from the U.S. Treasury, the 10-year yield yesterday, May 21, 2026, stood at 4.57%, while 20-year and 30-year yields were already above 5% - at 5.09% and 5.10%. That means 5% is no longer some distant apocalyptic line from theoretical debates, but a zone into which the U.S. debt market has already partly moved. In that sense, the question is not only whether the 10-year will cross 5%, but why the entire long-term yield curve has moved so high, and why the market is no longer satisfied with the old assumption that U.S. debt is always an unconditional safe haven.

The first problem is fiscal. The United States is not borrowing exceptionally, like a state temporarily financing a crisis, but structurally. The Congressional Budget Office projects a deficit of 1.9 trillion dollars in fiscal year 2026, rising toward 3.1 trillion dollars by 2036, and an increase in debt held by the public from 101% of GDP to 120% of GDP. More importantly, net interest costs are expected to rise from 3.3% of GDP in 2026 to 4.6% of GDP in 2036. A reminder: net interest is the money the state pays simply to service old debt. It is not a new road, hospital, school, or industrial program. It is the price of past decisions.

This is where 5% becomes politically explosive. If a state has little debt, high interest rates are unpleasant but bearable. If it has enormous debt, high interest rates become a mechanism for disciplining the whole society. Let us explain, because the matter is actually very simple: an increasing share of the budget goes to creditors, while ordinary citizens are told there is not enough money for social programs, public services, or infrastructure. Financial capital thus receives a double privilege: first, it profits from the state when the state saves the system, and then it profits again when it charges the state interest on the debt created to maintain that very system.

The second problem is the real economy. According to Freddie Mac, the U.S. 30-year fixed mortgage rate stood at 6.51% on May 21, 2026, up from 6.36% a week earlier. For the average family, this is no longer an abstract Wall Street number. It means a higher monthly payment, less affordable housing, and the further locking out of a generation already living in an economy of high rents, expensive healthcare, and insecure work. When bond yields rise, the whole "reality" is in trouble, especially for workers who are not engaged in financial investing at all.

The third problem is "repricing", meaning the revaluation of almost everything. After 2008, the world got used to cheap money. Central banks lowered interest rates, bought bonds, and inflated the value of financial assets. That system did not produce stable prosperity, but a deep dependence on liquidity. Stocks rose, real estate rose, private capital expanded, and debt came to be seen as something that could be endlessly rolled into the future. But when long-term U.S. yields approach 5%, that future suddenly presents the bill.

5% is an extremely important number, but we should not understand it too mechanically. The point is not that the "world will collapse" the moment the figure moves from 4.99% to 5.00%. The point is that 5% symbolizes the end of an illusion: the illusion that America’s deficit, wars, spending, tax privileges for the rich, and monetary dominance can be financed without a serious cost. The bond market, indifferent and without ideology, is beginning to charge for what politics does not want to admit.

Numbers and Context

Many may now want to follow this figure from the political angle as well. You can do that here.

But if you expand the chart to "max", you will see that in the 1980s the yield was once far above 5%, and you might conclude that we are spreading unsupported alarmism. That is not the case, but we still need to explain why "today" and "then" are not the same thing.

As the chart above shows, in the 1980s yields of 10%, 12%, or 14% were dramatic, but they were acting on a different "organism" than today. The number was higher, but the system was different.

The most important difference is the combination of debt, inflation, and expectations.

In the 1980s, American interest rates were high because the United States was emerging from the inflation crisis of the 1970s. Paul Volcker, then chairman of the Federal Reserve, deliberately raised rates brutally high in order to break inflation. This was the so-called "Volcker shock": a consciously induced monetary tightening that pushed the economy into recession, but sent the market a message that inflation would be crushed at any cost. The Fed’s official history marks 1979 precisely as the turning point toward aggressive anti-inflation measures.

So a 13% yield then did not mean the same thing that a 13% yield would mean today. Why? Because inflation was also enormous at the time. If the nominal yield is 13% and inflation is 10%, the real yield, meaning the yield after inflation, is not 13%, but around 3%. That is why one must always distinguish between nominal yield and real yield. The nominal yield is the number we see on the screen. The real yield is what remains once inflation is subtracted.

What is the difference between then and now? Inflation today is elevated, but it is not at the levels of the early 1980s. If the 10-year is around 4.5% or 5%, and inflation is around 3%, the real yield is already quite heavy for an economy that has grown used to nearly free money. This is not Volcker’s world, in which brutal interest rates were used to break an inflation fever. This is the world after 2008, after quantitative easing, after the era of zero rates, in which the state, corporations, the housing market, and the stock market learned to live on cheap debt.

The second difference is debt. In the early 1980s, U.S. public debt relative to GDP was incomparably lower than today, only around 25–26% of GDP. Today, as we have already said, the CBO projects debt at around 101% of GDP in 2026, rising toward 120% by 2036. That changes the entire mathematics. If a state owes relatively little, it can withstand high interest rates for a while. If it owes roughly the size of its entire annual economy, even moderately high interest rates become a budgetary weight.

That is why today’s 5% is more dangerous than it first appears. Not because 5% is historically high. It obviously is not. The problem is that today’s 5% lands on a much larger debt pile and a far more financialized economy.

The third difference is the structure of the economy. In the 1980s, the U.S. economy was already transitioning toward the neoliberal model, but it was not yet as deeply financialized as it is today. Today, almost everything depends on the price of capital. Another reminder: "financialization" means that an ever larger part of economic life is not tied to the production of goods and services, but to asset prices, debt, credit, securities, and investor expectations. In such a system, a change in the yield on U.S. Treasuries is not just a change in one interest rate. It is a change in the entire gravitational field.

The geopolitical aspect must also be mentioned. In the 1980s, the United States, despite its crisis, was entering a phase of renewed hegemony. The Soviet Union was weakening, the dollar remained the central currency of the world, and the American financial market was becoming a global magnet. Today, the United States still possesses an enormous financial and military center of power, but it no longer has the same aura of irreversible ascent. China is a serious industrial competitor, dedollarization is moving slowly and unevenly, but it exists as a process, and American political polarization no longer looks to the market like folklore, but like fiscal risk.

There is one more important thing: in the 1980s, high interest rates were an instrument for restoring confidence. Today, high interest rates increasingly look like a symptom of declining confidence. That is a huge difference. Volcker raised rates to convince the market that the state and the Fed controlled inflation. Today, the market may demand higher yields because it is no longer sure that Washington controls the deficit, the political system, war commitments, or the long-term stability of the dollar.

That is why 5% today is not "higher" than 13% was then in a mathematical sense. But it may be more dangerous in a systemic sense. The number is smaller, but it falls on a much larger structure.

To conclude. As is usually the case in the world of economics and finance, one cannot look at a single number in a vacuum and turn it into a final forecast. There are connected indicators that only together explain the whole picture. But if you keep all that in mind, then you may freely take this 5% ceiling seriously, because it is serious. Could Trump’s armada begin withdrawing from the Persian Gulf and the Caribbean at 5%? From Taiwan, it seems, he is already stepping back. It could, yes.

Sources

- Cbo.gov The Budget and Economic Outlook: 2026 to 2036 https://www.cbo.gov/publication/62105

- Associated Press Average US long-term mortgage rate climbs to 6.51%, highest level in nearly nine months https://apnews.com/article/76e8188826180c65520a3c349505a42b

- Barrons.com Weekly Mortgage Rates Hit 6.51%, Highest Level Since August https://www.barrons.com/livecoverage/stock-market-news-today-052126/card/weekly-mortgage-rates-hit-6-51-highest-level-since-august-ZMVY2rnk0KgDoFdSW3gW

- Marketwatch.com Mortgage rates jump to over 6.5% — the highest level since the Iran war started https://www.marketwatch.com/story/mortgage-rates-jump-to-more-than-6-5-the-highest-level-since-the-iran-war-started-41728b4e

- Freddiemac.com Mortgage Rates https://www.freddiemac.com/pmms

- Fred.stlouisfed.org Market Yield on U.S. Treasury Securities at 10-Year Constant Maturity, Quoted on an Investment Basis https://fred.stlouisfed.org/series/DGS10

- Pgpf.org Interest Costs on the National Debt https://www.pgpf.org/programs-and-projects/fiscal-policy/monthly-interest-tracker-national-debt/

- Tradingeconomics.com US Mortgage Rates Hold Rebound: Freddie Mac https://tradingeconomics.com/united-states/30-year-mortgage-rate/news/550819

- Federalreservehistory.org Volcker's Announcement of Anti-Inflation Measures https://www.federalreservehistory.org/essays/anti-inflation-measures

Comments