Financial crises are most often remembered for days of panic. Unfortunately, we know what that looks like, and in case we have forgotten, the coming crisis triggered by the U.S.-Israeli aggression against Iran will soon serve as a reminder. But whether crises are caused, or rather exposed, by catastrophic miscalculations such as Trump’s current one, or whether they arrive as the inevitability of the existing economic order, one thing is always true: they come. We live in a world of cyclical, and increasingly frequent, crises.

But the real question should be asked much earlier, in the years when almost no one speaks of danger. In the years when loans are being repaid on schedule, asset prices are rising, banks are reporting profits, and politicians, as usual, claim that the economy has entered a new, "more mature phase". One economist precisely exposed the illusion of "quiet times" and gives us answers about what is coming.

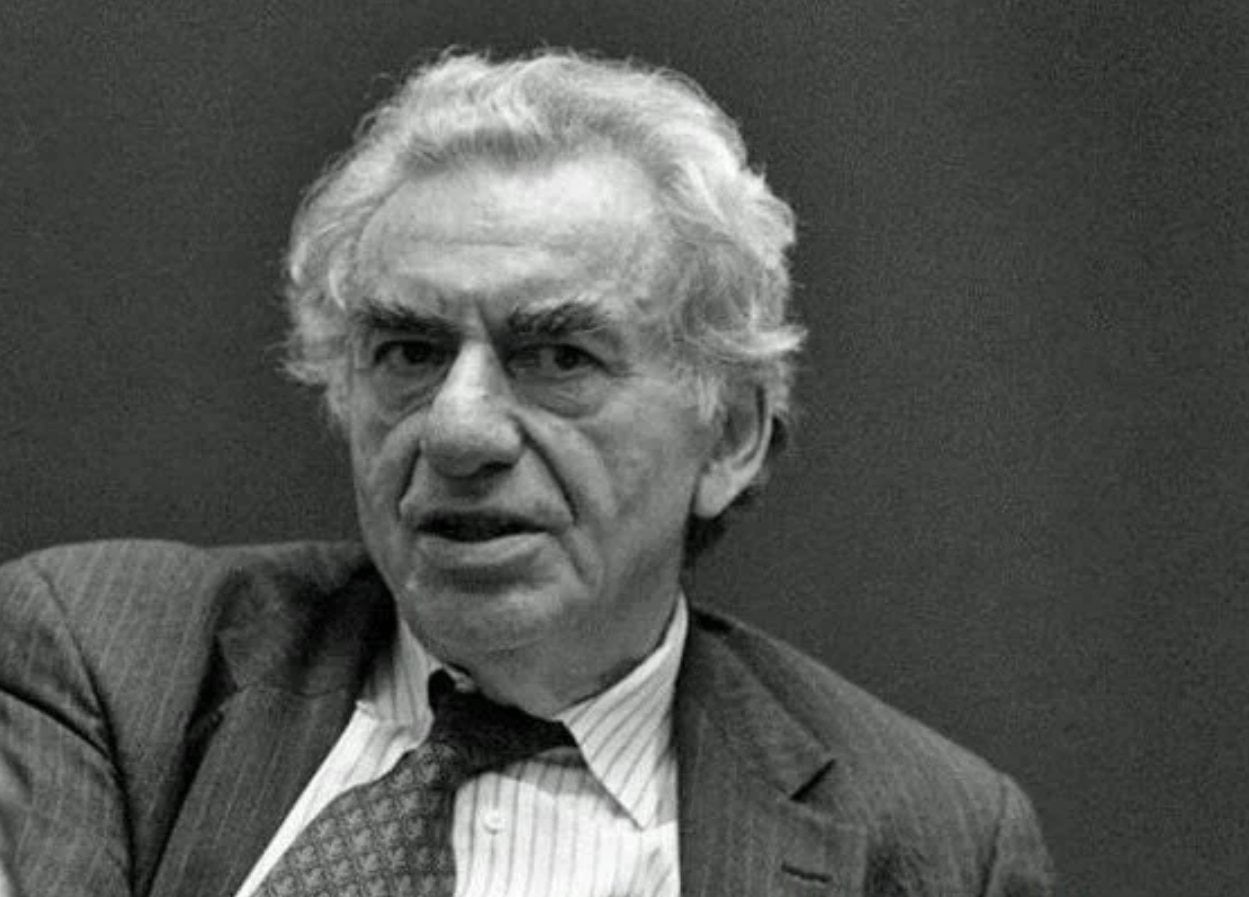

That economist was Hyman Minsky, an American economist who long stood outside the center of academic fashion. Minsky saw the most important signal precisely in that calm. His financial instability hypothesis rests on a simple but deeply uncomfortable idea. Stable times change people’s behavior. After enough years without a major collapse, caution begins to look old-fashioned. Debt seems more acceptable. Risk appears smaller. Banks approve loans more easily, investors search more aggressively for yield, and regulators find it increasingly difficult to justify strictness politically.

Minsky (1919-1996) understood capitalism as a system that carries crisis within its own mode of expansion. In his interpretation, financial collapse does not come only as the consequence of war, an oil shock or some sudden political catastrophe. The problem itself always grows from within, through contracts, balance sheets, expectations and optimism that over time turns into false confidence. When the market rewards risk for a long time, more and more actors begin behaving as if risk has been overcome.

That is the strength of Minsky’s thought. He does not look for catastrophe outside the system, because it is already built into the system itself. Minsky looks at the quiet years and asks what is really accumulating inside them.

The Economist Who Waited for the Crisis

Minsky was a man of serious intellectual genealogy. He studied at Chicago and Harvard, was influenced by Joseph Schumpeter and Wassily Leontief, and later spent much of his career far from the spotlight that shone on economists aligned with faith in efficient markets. At a time when models increasingly emphasized rational expectations, equilibrium and the ability of markets to allocate risk by themselves, Minsky insisted on finance itself as a source of disruption.

The longer the system holds, the more people conclude that it can bear a little more leverage, a little more refinancing, a little more delay...His thinking had an older predecessor in Irving Fisher. After the crash of 1929, Fisher developed the theory of debt deflation. When an economy becomes overindebted and then begins panic deleveraging, the sale of assets pushes prices down. Falling prices increase the real burden of debt. Debtors then have to sell even more, and the crisis deepens through its own logic. Fisher learned that lesson personally as well. As an investor, he lost a vast fortune in the market collapse, so his theory was not an academic exercise. It was the intellectual processing of a catastrophe he had felt himself.

Minsky carried that old story about debt into modern financial capitalism. His famous division into three types of financing sounds technical, but it actually describes the moral and psychological history of every boom. In the first phase, which he calls hedge financing, the borrower can pay both interest and principal from their own income. In the second phase, speculative financing, the borrower can pay the interest but must constantly refinance the principal. In the third phase, Ponzi financing, maintaining the debt depends on new borrowing or on the constant rise in the price of the asset.

That scheme describes a shift in social mood. At first, credit is taken because there is income to support it. Then credit is taken because the debt can be rolled over. Finally, credit is taken because everyone believes the asset will be worth more tomorrow. Stability, in this story, is the teacher of risk. The longer the system holds, the more people conclude that it can bear a little more leverage, a little more refinancing, a little more delay. The problem, as you have probably noticed, is that everyone in every phase thinks the same way, or at least very similarly.

How Caution Turns Into a Casino

Perhaps these are certain "truths" that, from today’s perspective, already seem familiar to us. But the fact that Minsky "knew" earlier what we learn only later is not merely confirmation of the accuracy of his forecast. It is also confirmation of the greater accuracy of what we today, let us put it this way, suspect with increasing confidence to be true.

After every catastrophe come laws, restrictions and guardrails "so it never happens again". But after a long peace, pressure grows to remove those guardrails.One of those truths is the fact that "good times" create their own ideology. In it, debt becomes a tool of growth, while financial innovation acquires an almost technocratic aura of intelligence. Banks develop products that promise to disperse risk. Investors accept increasingly complex instruments because there is too little yield in the "safe zones". Rating agencies, through their grades, turn complex packages of debt into goods suitable for global sale. Politicians always love a boom, and are not particularly interested in where it comes from, because it brings employment growth, tax revenues and a feeling of prosperity.

A large part of contemporary capitalism is driven by funds, asset managers, pension funds, hedge funds and vast institutions that manage other people’s capital. But their horizon is often short. Returns are calculated constantly, and falling behind competitors is punished quickly. In such a world, an individual manager can make seemingly rational decisions within his own mandate, while the system as a whole becomes ever more fragile.

Regulation also moves in cycles. After every catastrophe come laws, restrictions and guardrails "so it never happens again". But after a long peace, pressure grows to remove those guardrails. The American Glass-Steagall Act of 1933 was born out of the Great Depression and separated commercial from investment banking. Gramm-Leach-Bliley in 1999 symbolized a different era, one in which it was believed that financial markets were sophisticated enough to manage risk by themselves. The history of regulation therefore often looks like a pendulum swinging between fear after collapse and confidence before the next boom.

Financial innovation in such an environment becomes a double-edged sword. It can genuinely broaden access to capital and reduce some individual risks. At the same time, it can produce a labyrinth in which no one can see where the risk has stopped. This is precisely Minsky’s terrain. He observes the moment when safety becomes habit, and habit becomes blindness.

Minsky and 2008

After 2008, Minsky, predictably, became an unavoidable name in discussions about crises. Institutions that had long spoken only of market efficiency began talking about systemic risk, financial cycles and the danger of excessive leverage. Part of his diagnosis entered the technical vocabulary of central banks and international institutions. But we may ask what purpose all of that served. Because the "curse" Minsky clearly detected remained and keeps repeating itself. In other words, the system can learn the language of caution and then continue producing the conditions in which caution is once again exhausted.

Today’s Minsky moment probably would not look like 2008. American households at the end of 2025 did not carry the same debt-servicing burden as they did on the eve of the mortgage collapse. The debt-service ratio stood at around 11.32%, significantly below the level of 2007. But risk is now found at other addresses: in non-bank finance, commercial real estate, repo markets, hedge funds, crypto euphoria and technology bubbles, AI for example, though not only AI, fed by promises of future revolutions.

The global context sharpens the picture. World debt stands above 235% of global GDP, while the non-bank financial sector, meaning all financial institutions that are not traditional banks but also lend money or invest, such as investment funds, pension funds or hedge funds, accounts for around 51% of total global financial assets. This means that an enormous part of financial life takes place outside the classic image of a bank with deposits and loans. Capital moves faster, instruments are more complex, and the links between actors often become clear only when pressure rises.

In practice, these are large funds managing other people’s money, pension funds holding workers’ savings, insurance companies, funds lending money to firms, investment funds into which citizens and institutions invest, but also more aggressive players such as hedge funds. They are not the bank into which a citizen walks to open a current account, but they can have enormous influence over where money goes, under what conditions, how much risk is taken, and what happens when the market suddenly becomes frightened. That is precisely why the problem is not only in the banks we see on the street, but also in the vast financial space behind them, where money moves faster than the public can follow.

A Minsky moment should therefore be understood as a moment of recognition. It is the moment when society realizes that what it called stability was in fact the accumulation of obligations beneath a calm surface. The collapse becomes visible in a single day, but it is prepared over years. In credit contracts, in risk models, in bonuses, in political speeches about growth, in the belief that refinancing will "always be available" and that the prices of key assets can continue rising long enough for everyone to "get out in time".

The most dangerous sentence of every financial age is that this time is different. Minsky teaches us that this claim usually arises after a long period of success. A system that avoids crisis for a long time begins to behave as if it has outgrown crisis. That is where its deepest weakness hides.

Minsky and Marx

At first glance, Hyman Minsky and Karl Marx belong to different worlds. One writes about credit cycles and banks, the other about labor, capital and the social relations of production. Yet when their ideas are placed side by side, a deep kinship appears in the way they understand crises. Both see capitalism as a system that carries its own tensions within itself, and those tensions eventually rise to the surface.

Crises are not accidental malfunctions to be repaired, but consequences of the system’s normal functioning.For Marx, the driver of crisis lies in the process of capital accumulation. Firms must constantly expand production, seek higher profit and compete in the market. In that process, capital becomes concentrated, pressure on labor increases, and periodic surpluses of production appear that cannot be absorbed through consumption. The system then enters recurring phases of disruption, because the logic of growth does not stop operating after a crisis.

Minsky looks at the same system from the financial angle. His focus is debt, credit and the way investment and consumption are financed. In stable periods, financing gradually shifts from safer forms to riskier ones. More and more actors rely on refinancing and rising asset prices. The system then becomes sensitive to changes in interest rates, confidence and liquidity. Crisis breaks out when that chain begins to snap.

The similarity between the two becomes clear at one crucial point. Crises are not accidental malfunctions to be repaired, but consequences of the system’s normal functioning. For Marx, capitalism produces imbalances through its own need for expansion. For Minsky, the financial system produces collapse through its own need for credit and profit. In both cases, stability does not remove the problem, but often deepens it.

The Persian Gulf as Trigger

The current escalation in the Persian Gulf gives Minsky’s logic a very concrete contemporary framework. An energy shock in a highly indebted world does not affect only the price of fuel. It immediately pressures production costs, transport, food, inflation and interest-rate expectations. If the war deepens, the shock will not remain merely geopolitical. It becomes a financial stress test.

The key danger lies in the combination of an energy disruption and a system that already lives on refinancing. Companies with thin margins, states with high public debt and financial actors outside the traditional banking sector would feel the pressure first. A rise in energy prices can quickly consume liquidity, crush expected profits and open the question of who can still service debt properly at all.

That is why the Persian Gulf today is not just another war, but an accelerator of an already existing weakness. A Minsky moment rarely begins with the shock itself. The shock only reveals how expensive, indebted and dependent on the assumption of continuing normality the stability before it really was.

The Moment Before Admission

Today’s moment clearly no longer looks like "stability" to anyone, but neither is it yet an open financial collapse. Inflation has already changed everyday life, interest rates have returned as a serious cost, debts are more expensive, and wars and energy shocks have become the permanent background. People therefore have good reason to feel that a crisis is approaching. This is an interesting and uneasy moment: its conditions are already here, even though it has not yet taken its final form.

Minsky’s logic helps us understand precisely this interim phase. A crisis does not begin only when banks fall or markets sink. It begins earlier, when debts are still being serviced, but with increasing difficulty. When loans are still being refinanced, but on worse terms. When the system still functions, but with far less room for error.

The Persian Gulf can be one of the triggers because more expensive energy quickly raises the costs of transport, food and industry. That feeds inflation, inflation pressures central banks, and higher interest rates hit debtors. The chain is simple and dangerous.

The crisis therefore now seems almost certain in the broader sense. The only open question is its form. It may be financial, energy-related, debt-driven, inflationary or, worst of all for all of us, combined. It may stretch out for years as a slow impoverishment, or condense into a few dramatic weeks. We are in the moment before official recognition, when many already feel the crisis, while institutions still do not want to declare it. Still, the acceleration of bad news, especially from the Persian Gulf, means that both the declaration and the recognition are now very close.

Sources

- Fraser.stlouisfed.org The Debt-Deflation Theory of Great Depressions https://fraser.stlouisfed.org/title/debt-deflation-theory-great-depressions-3596/fulltext

- Federalreservehistory.org Financial Services Modernization Act of 1999 (Gramm-Leach-Bliley) | Federal Reserve History https://www.federalreservehistory.org/essays/gramm-leach-bliley-act

- Levyinstitute.org Minsky Crisis https://www.levyinstitute.org/publications/minsky-crisis/

- Nber.org Corporate Debt, Boom-Bust Cycles, and Financial Crises https://www.nber.org/papers/w32225

- Arxiv.org Minsky Financial Instability, Interscale Feedback, Percolation and Marshall-Walras Disequilibrium https://arxiv.org/abs/1402.0176

- Pimco.com Some Unpleasant Keynesian Minsky Logic | PIMCO https://www.pimco.com/us/en/insights/some-unpleasant-keynesian-minsky-logic

- Ideas.repec.org The Anatomy of a Typical Crisis https://ideas.repec.org/h/spr/sprchp/978-3-031-16008-0_2.html

- Levyinstitute.org The Financial Instability Hypothesis https://www.levyinstitute.org/publications/the-financial-instability-hypothesis/

Comments